A Guide to your Savings Rate (Sr)

What is it?

Savings Rate (Sr) is the percentage of your annual gross income being saved for future use.

Example: Assume your annual gross income is $200,000. If you save $20,500/yr into a 401(k), $10,000/yr into a brokerage account, and $5,000/yr into a 529, your Savings Rate (Sr) is 17.75%.

Why does it matter?

Savings Rate (Sr) tells an important story about your current financial wellness and progress towards financial independence.

Sticking to a meaningful and realistic Sr is highly correlated to financial independence. Set a goal, save the right amount of money each year, and don’t give yourself a pass. For most, Sr is probably the single most important indicator of long-term success. It allows you to measure the flexibility in your plan and feel more prepared for financial setbacks as a higher Sr provides more cushion for unexpected liquidity needs.

Sounds simple, but In reality we struggle to save money for the future because humans, by nature, tend to have a behavioral tendency called “Present Bias”. This means that we tend to favor payoffs that are closer to the present than in the future and also means we tend to spend before saving.

As a result, our lifestyle and consumption choices are by far the biggest variables impacting savings rates. Where we choose to live, the car we choose to drive, the foods we choose to eat, and where we choose to send our kids to school directly impact our ability to save. Our modern economy is also in competition with our ability to save by making it easier than ever to subscribe to more services and buy more things to be delivered to our door.

The key ingredient here is choice. We choose our lifestyle and what we consume. If we want to maintain a healthy Sr we must make (sometimes hard) choices about what to spend our money on. Ideally, we understand our values and what matters most in our lives so we can spend generously on things that matter and be frugal with things that don’t. Save first, spend on what matters, reduce what doesn’t.

Do I have a good Savings Rate (Sr)?

In order to determine if your Sr is “good” for your unique life circumstances and make appropriate adjustments, we’d suggest the following steps:

- Score Accuracy - Confirm the inputs to determine your Sr are accurate

- Score Assessment - Determine whether your Sr is appropriate

- Score Improvement - Identify obstacles and areas for improvement

Score Accuracy

Step 1 - Confirm Recurring Contributions

Look at your various accounts (Savings, IRA, 401(k), 529, etc) and confirm what contributions happen automatically on a recurring schedule. Depending on manual savings is one of the ways we end up letting ourselves off the hook. While we may have every intention to save our bonus or transfer that money to savings, the reality is that our bonus is not guaranteed nor is our ability to resist splurging if it does come in. Contrast this with our 401(k) contribution where the savings happens with every paycheck with zero effort or additional temptation to resist on our part.

Step 2 - Add Extra Debt Payments

Do you make additional payments on your mortgage? Pay more than the minimum on your credit card? These extra debt payments are often overlooked but should be considered part of your Sr. Anything that has a direct and positive impact on your net worth, like an extra debt payment, should be considered part of savings. Making an extra debt payment also comes with a “guaranteed” rate of return, the interest rate of the debt being paid off which would otherwise compound negatively. Be mindful of your balance between additional debt payments and long-term savings as too much of either could be less than ideal.

Step 3 - Confirm Gross Income

An accurate Sr is dependent on knowing both how much you save and how much you earn. Did you get a raise this year? Take a pay cut to pursue a more fulfilling career? If your income increased this year, make sure you adjust your savings accordingly and avoid allowing your lifestyle expenses to subtly creep higher. If your income has decreased this year make sure your Sr isn’t too high (yes, that’s a thing!) and try to make sure you still take advantage of things like your employer match.

Score Assessment

To determine whether your Sr is appropriate it is important to understand:

- Understand Healthy Sr Score Ranges

- Understand Correlating Factors

Step 1 - Understand Healthy Sr Score Ranges

Healthy Sr scores generally fall between 10% and 30%.

There is no single Sr that is right for everyone. However, if your Sr is less than 10% it may be difficult to achieve financial independence. Conversely, if your Sr is greater than 30% you may be sacrificing your current lifestyle for an uncertain future. Where you fall between 10% and 30% could be influenced by many factors.

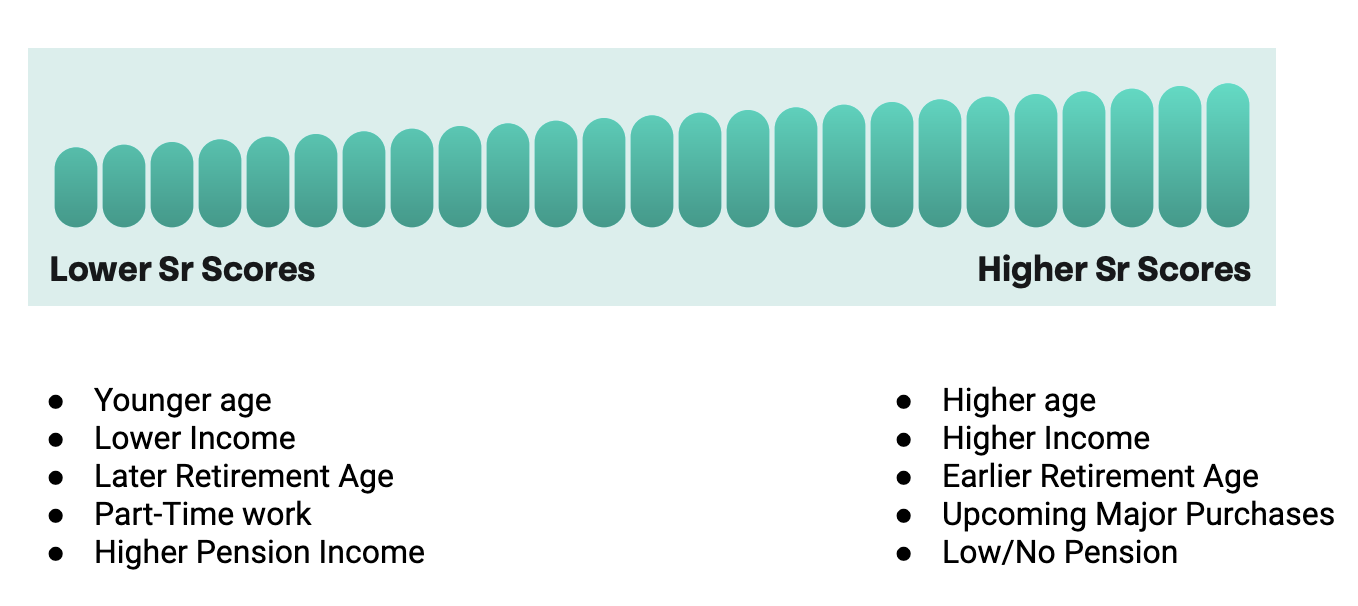

Step 2 - Understand Correlating Factors

Everyone has unique life goals and financial circumstances that influence their Sr. Understanding the most common correlating factors will help you understand your Sr and determine if it is appropriate.

Score Improvement

Improving your Sr can be broken down into two simple steps.

- Identify Obstacles to Saving

- Identify Strategies to Overcome Obstacles

Step 1 - Identify Obstacles to Saving

This step is simple, but not necessarily easy. Identifying obstacles to saving requires taking an honest look into our lives, our relationship with money, and being comfortable with uncomfortable truths. We must recognize that we may have made less than optimal money choices in the past but that we also have the power to make better choices moving forward. Common obstacles to saving include:

Limited Cash Flow - The biggest hurdle for many in saving is simply having the free cash flow to save in the first place. Don’t let yourself off the hook quite yet, there are different reasons that cash flow could be limited. Are your fixed expenses or debt payments taking up most of your income? Overspending? These are two distinct obstacles that require different changes to create the ability to save. Identify the real reason cash flow is limited so you can make the appropriate changes

Overspending - This can stem from a variety of things so it is critical to understand the root cause. Perhaps healthy spending or saving habits were never modeled in your household. Do you know what you are saving for and does it really matter? If the answer is no, you won’t have the conviction to save instead of spend. Are you “keeping up with the Jones’”? It’s easy to see a big home, fancy car, or nice clothes. It’s much harder to see if that lifestyle comes with financial security or a maxed out credit card. Decide what you want.

Lack of Education - We are never taught basic money fundamentals as any part of our formal education, so how are we supposed to learn it? We want to save in the “best way” but the issue is that there is no single best way and you have a lot of options to choose from. This can create a “I don’t know where to save so I just won’t save at all” mindset that hinders your savings goal. How much and how consistently you save is more important than where you save.

Market Fear - This is related to the obstacle above but important enough to state separately. For new savers/investors the short-term volatility can be downright scary and enough to avoid getting started. After all, why would you save/invest if you are just going to lose money?!

Debt Aversion - While making extra debt payments is part of your Sr, you can have too much of a good thing and sabotage your long-term financial independence. If you put all free cash flow toward debt reduction the end result is being tied to a job forever because you have no liquid savings and need to support your lifestyle through earned income

Step 2 - Identify Strategies to Overcome Obstacles

Once you’ve identified the real reasons your Sr is not appropriate you can take action to improve it. Here are some of the most common strategies to overcome them.

Save first, spend what’s leftover - Budgeting is overrated. Instead, determine how much you want to save and get it out of your account right away. This can be done through your 401(k) or setting up a direct deposit through your payroll so it goes right into savings and never touches your checking account. Most of us don’t need to budget, the amount of money in our checking account does this automatically. Keep it simple, save first and then live off whatever is in the checking account.

Out of sight, out of mind - Once you start saving it will be easier to stick to if you don’t see the balance on the same app as your checking account. It is far too easy to transfer money from savings to checking when that impulse moment comes. Recognize this human tendency and cut it off ahead of time by saving in a place that you don’t see everyday and it takes more than a couple clicks to access

Systematic and automatic - Make saving as easy as possible by automating it. It is far harder to save if you have to make a choice to do it every month by manually moving money from checking. Use your 401(k) or direct deposit to automate saving wherever possible. It changes the decision point. Instead of choosing to save, once you automate you have to choose not to save. This will increase your Sr.

Increase Income - Sr generally increases as income increases. The job you have today does not have to be the job you have tomorrow. Are you being paid at market rate for your work? Have you asked (nicely :) ) for a raise recently? Have you explored what other opportunities are available? Are you actively developing your personal skill set to become more valuable?

Make Hard Choices - Sometimes the reality is the only way to start saving more is to reduce overhead. Perhaps you bought the house at the very top of your budget or splurged on the luxury car. Home and car purchases are not permanent. These types of choices aren’t easy, but they are doable if you have a meaningful reason to increase your savings.

Education/Accountability - If not knowing where to save or concerns about the market are holding you back, take time to learn so you feel comfortable. There are great online resources available or you could talk with a friend or mentor that you view as having expertise in this area. If talking with someone you know personally about money doesn’t feel great then consider working with an independent financial planner who will educate you on your options and act as a trusted guide and accountability partner to hit your savings goals.